“Sea Point, Cape Town investment properties are at the tip of the tongue in the real estate investment world in South Africa at the moment. Everyone wants a piece of luxury real estate by the seaside with property prices surging and the increased demand for apartments in the area. This got me thinking about the financial projections and the better investment between a luxury, Sexy Sea Point property, and a property portfolio in a more modest middle-class area with a similar budget.

Before we begin the analysis, remember that the investor’s objectives deeply influence an investment strategy. For instance, one might consider acquiring a Sea Point property, aiming for long-term ownership to capitalise on value growth, while another investor might focus on properties in areas, prioritising immediate cash flow.

Utilising the available data, we can conduct a nuanced comparison of the financial viability between investing in a single upscale apartment in Sea Point and purchasing several properties in the more moderately priced Parklands area. Let’s look at the numbers for each property:

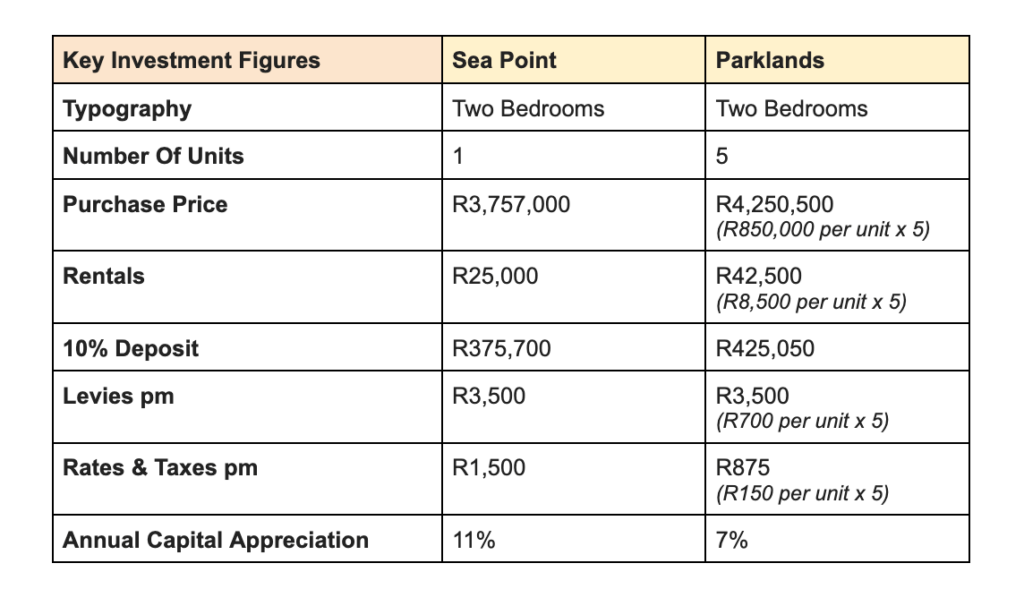

INVESTMENT COMPARISON OVERVIEW

FINANCIAL COMPARISON

1. Initial Capital Outlay

The initial capital outlay is a 10% deposit for each property. Comparatively, the 5 Parkland Properties equate to a higher total purchase of R4,250,000 vs R3,757,000 for the Sea Point Property. As a result, the initial outlay for Parklands is R49,350 more (R425,050 – R375,700).

2. Cash Flow Analysis

Cash flow analysis is vital for assessing an investor’s financial health, determining the viability of investments, and guiding strategic decision-making. It helps identify a surplus or shortfall of funds by considering the income and expenses.

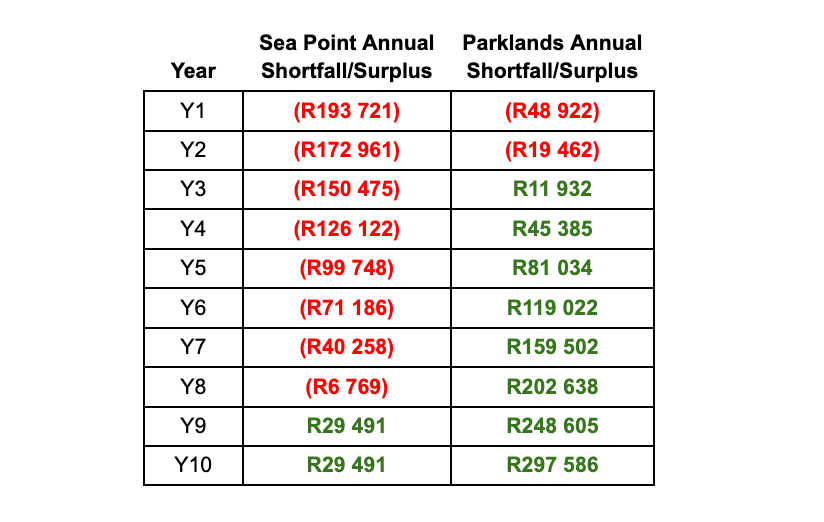

Let’s look at the cash flow of each of these investment decisions over 10 years by taking the rental income annually and deducting the annual expenses (levies, rates and taxes + bond repayments) to determine in which year the investor will be generating positive cash flow:

The Sea Point apartment becomes cash flow positive in Year 9, meaning it takes nine years for the rental income to exceed all expenses and financing costs. In contrast, the Parklands units achieved cash flow positivity in Year 3. The investor who chooses the Sea Point property must ensure they have enough capital to invest in the property to cover the shortfalls for 9 years R861,240 vs the two years of shortfall for Parklands of R68,384.

This quicker turnaround for the Parklands properties is significant for investors who prioritise early returns. The properties that are cash flow positive earlier provide immediate income and can cover their expenses sooner. This can improve an investor’s qualifications for loans, making it an essential tool for scaling a property portfolio and optimising investment returns to ensure long-term sustainability.

3. Risk and Diversification

Another important factor when considering cash flow and managing your money is that the property may not have a 100% occupancy rate. With five separate income-producing assets in Parklands, investors spread their risk. A vacancy in one unit has a smaller impact on the overall income stream compared to a single high-value unit in Sea Point, where a vacancy can result in a total loss of income until a new tenant is found.

4. Appreciation and ROI

Sea Point offers a higher capital appreciation at 11% versus 7% for Parklands properties. A higher growth rate must be weighed against the extended period to reach cash flow positivity. However, they may not appreciate as quickly in value, potentially offering lower long-term gains. The choice depends on whether an investor prefers immediate income or is willing to wait for potentially higher returns through property value increases. Investors must consider their goals and their preferred weighting between capital appreciation and cash flow. We can see further insight into this by looking at the equity and return on investment on each property over 10 years.

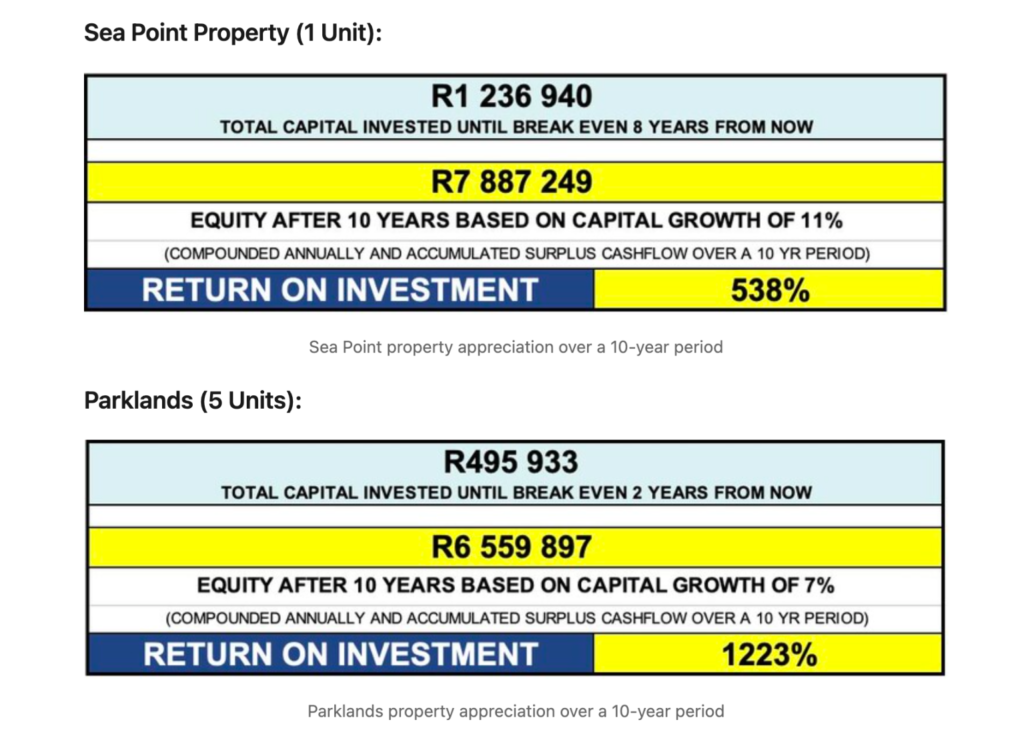

To calculate the Return on Investment (ROI), we first sum the total cash investment anticipated from the investor over 10 years, including both the initial deposit and any subsequent shortfalls. Next, we assess the property’s value, representing the investor’s equity, and factor in the appreciation and growth achieved by each property over the decade, along with any surplus generated from rental income. This comprehensive approach allows us to determine the ROI.

There is a significant difference in the return on investment with the Parklands Properties achieving much higher returns.

5. Tax Incentives

In addition to the above, investors who have purchased 5 new properties as per the multiple-unit strategy in Parklands will qualify for Section 13 tax incentives, offering a 55% tax deduction on the purchase price (R2,337,500). This has a substantial impact on the returns and one’s investment strategy. This is cash in your pocket to subsidise your investment portfolio through your annual tax deduction with SARS.

CONCLUSION

Although the Sea Point property might be in a more prestigious location with a higher rate of capital appreciation, the data suggests that the multiple units in Parklands or middle-class markets could be a smarter choice for investors seeking early cash returns and lower risk through asset diversification.

When comparing the two investments, the Parklands units present a compelling case for investors looking for earlier cash flow positivity, risk diversification, and substantial tax benefits. The quicker cash flow positive status of the Parklands units makes them an attractive option for generating revenue that can be reinvested. The high Section 13SEX tax benefits further sweeten the deal, offering considerable savings that enhance overall profitability. This leaves me with a final thought that the best investments might not always be the most sexy.”